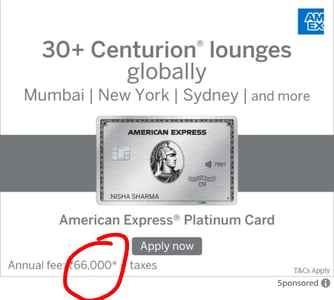

Is This American Express Credit Rs 66000 Annual Fee Premium Luxury or Just a Big Joke for Indian Consumers ?

The Indian digital space is buzzing with amusement after a sponsored advertisement popped up on Amazon India displaying a premium American Express credit card with an eye popping annual fee of sixty six thousand rupees plus taxes. For the average retail consumer browsing for monthly groceries or mid range electronics a recurring financial charge of that magnitude feels entirely disconnected from reality. This premium product is essentially a charge card aimed at the top one percent of income earners such as corporate executives and wealthy global business travellers who seek luxury travel perks. For the typical domestic customer who expects a payment card to be free or cost a nominal amount the advertisement looked like an unintended piece of financial comedy on their shopping screens.

The core irony driving the consumer reaction comes down to practical everyday usability across local market conditions where American Express faces a massive acceptance crisis. Step into a local clothing store an offline electronics dealer or try using it on smaller online transactional portals and this premium card is routinely rejected. Shopkeepers actively avoid processing transactions on this network due to steep merchant discount rates that typically climb between two point five to three point five percent coupled with eighteen percent goods and services tax on the processing fees. For businesses operating on tight competitive margins parting with such a high slice of revenue just to receive money from a buyer makes no commercial sense especially when alternative payment networks clear funds faster without eating into retail profits.

This visible disconnect highlights the massive structural shift taking place across the native financial system where the indigenous RuPay network has recorded revolutionary growth numbers. Backed heavily by national financial authorities RuPay has captured nearly sixteen to eighteen percent of the total credit card market share by value with its transaction volume jumping to a staggering thirty eight percent of the total credit space. Having achieved over seven hundred and fifty million transactions worth more than sixty three thousand crore rupees in recent operational cycles RuPay cards have successfully integrated with the Unified Payments Interface platform allowing people to link credit accounts directly to mobile apps for instant quick response code scanning at over fifty million merchant points. This setup enables a user to walk up to a roadside tea stall or small corner shop and make a digital transaction for a minimal amount with absolute ease and near zero processing liability for the vendor.

When evaluating this scenario through a critical consumer lens the situation reflects a deep psychological divide within the current marketplace. The international brand relies heavily on premium prestige marketing offering elite hotel upgrades and exclusive airport lounge entries to justify its premium pricing. However the contemporary Indian customer prioritises high functionality widespread utility and direct value over traditional elite status symbols. While the premium card struggles to find acceptance even inside major urban shopping hubs due to high merchant fees the humble domestic network is rapidly capturing the entire economic landscape by democratising digital credit access. The massive online reaction to the advertisement proves that high status marketing gimmicks no longer impress mainstream retail consumers who demand practical usability in their financial tools.