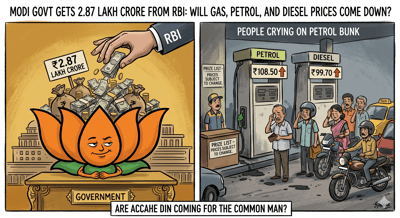

Modi Govt Gets 2.87 Lakh Crore From RBI: Will Gas, Petrol, and Diesel Prices Come Down?

The financial corridors of Mumbai witnessed a monumental decision that has triggered both admiration and intense public debate across the country. The Central Board of Directors of the Reserve Bank of India officially approved a staggering surplus transfer of 2.87 lakh crore to the central administration for the accounting year. Chaired by Governor Sanjay Malhotra during the landmark 623rd board meeting, this record breaking dividend payment marks a noticeable expansion over previous annual disbursements. For the Modi govt, this immense windfall provides unmatched financial leverage and massive breathing room to support state expenditure. Naturally, the arrival of such a vast sum has instantly led the public to expect sweeping consumer relief, with millions wondering if retail rates for essential commodities like petrol, diesel, and cooking gas will finally see steep price cuts.

However, historical patterns and administrative tendencies show that the likelihood of this wealth reaching the pockets of common citizens is incredibly slim. Over successive terms, state policy has consistently preferred keeping central taxes high on petrol and diesel rather than passing operational windfalls down to retail fuel pumps. This structural approach means that even when the national treasury experiences massive independent gains, consumer fuel prices remain stubbornly tied to volatile global market pricing and rigid local commercial marketing structures. Relying on an exceptionally high excise tax collection system has created a rigid dynamic where retail fuel pricing is rarely lowered to offer inflation relief. The current dynamic suggests that the leadership will likely retain these vast funds at the macro level to mask systemic revenue shortfalls rather than applying direct price reductions on fuel products.

Looking deeper into the state operational balance sheet exposes significant long term structural concerns regarding financial management and structural planning. The massive 2.87 lakh crore distribution is being celebrated as an independent triumph, yet it highlights an escalating institutional dependency on central bank earnings to disguise underlying fiscal weaknesses. Observers note that regular tax collections have faced continuous pressures, prompting the executive machinery to lean heavily on banking asset reserves to meet its annual budgetary targets. By absorbing almost the entire available net income of the central banking institution, the administration leaves the monetary authority with less internal room to navigate long term risks. While the board did allocate 1.09 lakh crore toward the internal Contingent Risk Buffer to satisfy formal guidelines, keeping the safety ratio at the lower bound of 6.5 percent indicates that long term financial cushion is being compromised to supply immediate state liquid cash.

In summary, this multi lakh crore transaction functions primarily as an administrative safety valve rather than a consumer benefit package. The state executive team is highly expected to channel these fresh billions into paying down existing market borrowings, financing capital heavy infrastructure, and handling standard welfare programs without introducing new public debts. While this strategy successfully keeps the overarching national balance sheet stable in front of global credit rating agencies, the everyday motorist and domestic household receive no direct relief from high living expenses. The choice to utilize central bank profits to fill systemic budget gaps allows the leadership to defer essential systemic tax reforms. As the new financial cycle progresses, this massive capital movement stands as a clear reminder that grand macroeconomic figures rarely translate into lower prices at the consumer fuel station.